At 2:17 p.m., the 400-ton hydraulic in Bay 3 is doing absolutely nothing.

Ram parked at top dead center. Operator staging parts. Main motor still spinning because that’s how the system stays ready. You can hear the hum over the forklifts. It’s been humming since 6:00 a.m.

That sound used to mean “bulletproof.” Now it sounds like a meter running.

Hydraulics still own the revenue charts. They held the largest market share last year and the overall press brake market keeps growing. On paper, that looks like validation: if they were margin killers, buyers would have abandoned them already.

But revenue share doesn’t measure what it costs you to keep 60 gallons of hydraulic oil hot, a 30–50 HP motor spinning, and a proportional valve stack fed with tariff-loaded spares. It just measures what you paid up front.

I’ve signed off on enough CapEx to know the trap. A 400-ton, 14-foot hydraulic with a global badge feels safe because it has 20 years of field history. The irony? The longer that architecture sticks around unchanged, the more it compounds energy inflation and parts pricing that never resets downward.

The machine didn’t get worse. The environment did.

The CapEx Reality: “Proven” only describes uptime — it says nothing about the cost structure you’re locking in for the next decade.

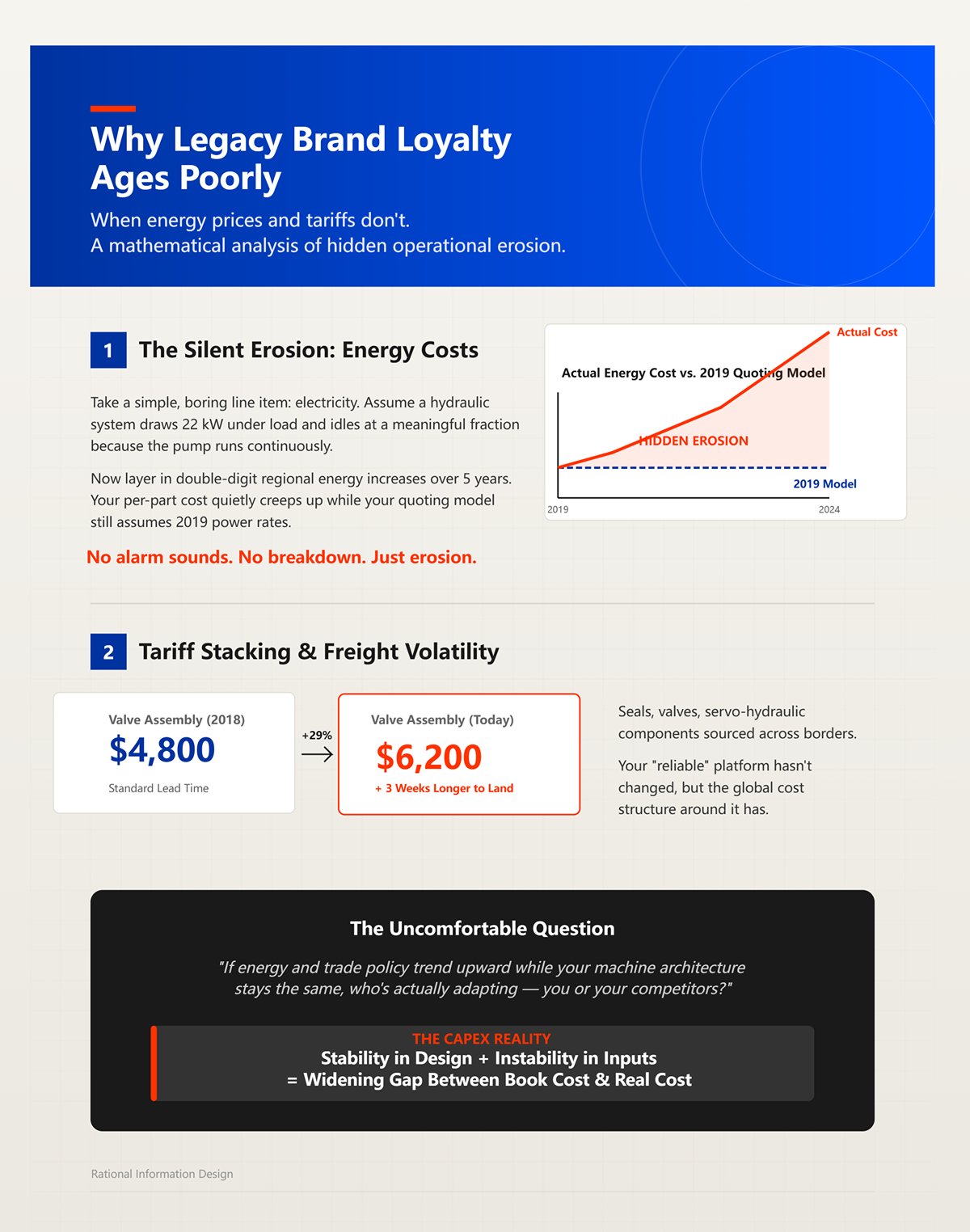

Take a simple, boring line item: electricity. Assume a hydraulic system draws 22 kW under load and idles at a meaningful fraction of that because the pump runs continuously. Now layer in double-digit regional energy increases over five years. Your per-part cost quietly creeps up while your quoting model still assumes 2019 power rates.

No alarm sounds. No breakdown. Just erosion.

Then parts. Seals, valves, servo-hydraulic components sourced across borders. Add tariff stacking and freight volatility. That $4,800 valve assembly you replaced in 2018 is $6,200 today and takes three weeks longer to land. Your “reliable” platform hasn’t changed, but the global cost structure around it has.

Brand loyalty made sense when input costs were stable and global supply chains were boring. They aren’t boring anymore.

And here’s the uncomfortable question: if energy and trade policy trend upward while your machine architecture stays the same, who’s actually adapting — you or your competitors?

The CapEx Reality: Stability in design plus instability in inputs equals a widening gap between book cost and real cost.

Let’s be fair. The giants aren’t asleep. The market is growing north of 7% year-over-year, and they’re still leading competitive matrices. Automotive alone throws off hundreds of millions in CNC demand, and high-tonnage hydraulics still dominate that space for a reason: they hit force targets all day.

If you’re bending 10 mm structural components in automotive volumes, uptime beats ideology.

But scale cuts both ways. Global manufacturing footprints mean exposure to the same tariffs and currency swings you are. Large installed bases mean backward compatibility expectations. When you’ve sold thousands of hydraulic platforms, radical redesign risks alienating your own service ecosystem.

That’s not incompetence. That’s inertia.

So when a 300-ton hybrid-electric arrives with comparable tonnage, lower idle draw, and software that doesn’t require a proprietary service laptop to tweak a parameter, the question isn’t whether the giants can respond.

It’s how fast they can pivot without cannibalizing their own golden geese.

The CapEx Reality: Market leaders can outspend challengers, but they can’t outmaneuver physics or policy without disrupting themselves.

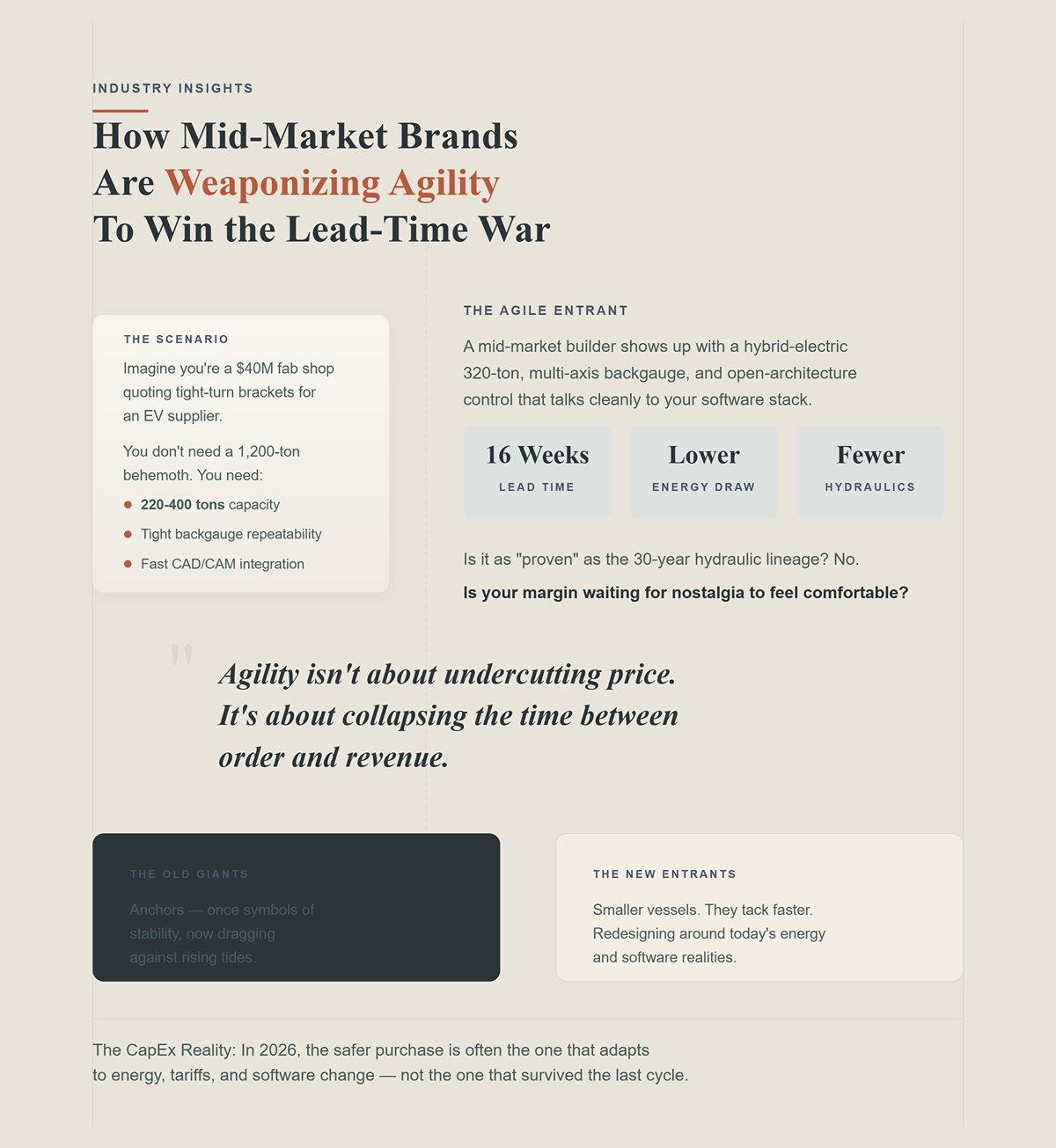

Now imagine you’re a $40 million fab shop quoting tight-turn brackets for an EV supplier. You don’t need a 1,200-ton behemoth. You need 220–400 tons, tight backgauge repeatability, and fast programming integration with your existing CAD/CAM.

A mid-market builder shows up with a hybrid-electric 320-ton, multi-axis backgauge, and open-architecture control that talks cleanly to your software stack. Lead time: 16 weeks. Energy draw at idle: dramatically lower because the motor isn’t spinning continuously. Fewer hydraulic components to source globally.

Is it as “proven” as the 30-year hydraulic lineage? No.

Is your margin waiting for nostalgia to feel comfortable?

Agility isn’t about undercutting price. It’s about collapsing the time between order and revenue, and shaving operating cost in the background while you focus on throughput. Smaller builders don’t have decades of hydraulic legacy to protect. They can redesign around today’s energy and software realities without apologizing to yesterday’s installed base.

The old giants are anchors — once symbols of stability, now dragging against rising tides. The new entrants are smaller vessels. They tack faster.

And if margin is the wind, which one do you want to be steering?

The CapEx Reality: In 2026, the safer purchase is often the one that adapts to energy, tariffs, and software change — not the one that survived the last cycle.

You’re standing in front of two quotes for a 320-ton, 12-foot machine with a 6-axis backgauge. One is a conventional hydraulic with a 30 HP main motor that runs whenever the machine is on. The other is a hybrid-electric: servo-driven pump, closed-loop control, motor only spins when the ram moves.

Both will bend 1/4″ A36 all day. Both hit your force targets. On paper, they look like peers.

Now put numbers on them. Assume the hydraulic averages 22 kW draw during production hours because the pump never truly rests. The hybrid averages closer to 10–12 kW because it’s not circulating oil at idle and only ramps when force is demanded. Run 2,000 production hours per year. That’s roughly 44,000 kWh versus 22,000–24,000 kWh.

At $0.14 per kWh, you’re looking at about $6,160 annually for the hydraulic and roughly $3,080 for the hybrid. Double the runtime to 4,000 hours — which isn’t crazy in automotive or appliance work — and now you’re staring at a $6,000+ annual delta.

Over ten years, that’s $60,000 before we even touch oil, filters, or valves.

And here’s the part legacy reps don’t like to say out loud: all-electric platforms are now reaching 500 tons, and emerging hybrids are pushing toward 800 tons. The old line — “Electrics are fine for light gauge, but real tonnage needs hydraulics” — is starting to sound like a rotary phone argument in a smartphone market.

The tonnage ceiling moved. Quietly.

The CapEx Reality: When a 300–500 ton hybrid-electric matches force output and cuts five figures off your 10-year energy spend, “hydraulics are safer” stops being technical and starts being emotional.

You’ve seen the brochure: “Up to 50% energy savings.”

Up to is doing a lot of work.

If you’re a two-shift shop running 3,500+ hours annually, with meaningful idle time between jobs, hybrids and full electrics absolutely deliver dramatic savings. The physics is simple: no continuous pump, no constant oil shear heating, no throttling losses across proportional valves. Power draw tracks actual ram movement. Energy scales with work performed.

But scale cuts both ways.

If you’re running 800 hours a year on a heavy 600-ton machine for thick plate jobs, most of that time is under load. The motor is working either way. Your idle savings shrink. The delta narrows. Suddenly that 40–70% headline number compresses into something closer to 15–25% in real dollars.

And then there’s distributed load. Apply full tonnage over 6 feet of a 10-foot bed and you’re asking for frame stress, whether it’s hybrid or hydraulic. Same with poor die selection. I’ve seen a 1/4″ A36 bend swing from 139 tons to over 300 tons just by tightening the V-die opening. If your process discipline is sloppy, no motor architecture will save you from overloading and the maintenance that follows.

Energy savings are real. But they’re conditional — on duty cycle, on process control, on actual utilization.

Which means the smart buying question isn’t “Is it 50% more efficient?” It’s “At my annual hours and mix, what is the 10-year delta in dollars?”

The CapEx Reality: Energy savings are not a slogan — they’re a function of your runtime profile. Run the kWh math against your real hours or you’re just buying optimism.

Picture year seven of ownership. Your hydraulic brake is fully depreciated on paper, but it’s still in production. Oil changes, filter swaps, seal kits — all standard. Then your state tightens environmental reporting around industrial fluids. Waste oil handling costs tick up. Documentation requirements increase. Insurance riders adjust.

None of that shows up in the OEM brochure.

A hydraulic system carries 40–80 gallons of oil. That’s a spill risk, a disposal cost, and a compliance obligation for the life of the machine. Hybrids reduce volume significantly. Full electrics eliminate it.

Depreciation schedules assume regulatory stability. ESG policy doesn’t care about your accounting timeline.

And let’s talk parts. Proportional valves, servo-hydraulic components, seal kits — many are globally sourced. Add tariffs and freight volatility, and your $4,800 valve becomes $6,200 with a longer lead time. When your platform depends on a dense hydraulic ecosystem, you are exposed to every geopolitical hiccup that touches fluid power components.

Remove oil, and you remove an entire failure tree: contamination, leaks, heat degradation, pump wear. You don’t eliminate maintenance. You shift it toward motors, drives, and encoders — components that are increasingly standardized and domestically stocked.

The question stops being “Which is more proven?” and becomes “Which architecture carries less regulatory and supply-chain drag over 10–15 years?”

The CapEx Reality: If ESG rules tighten faster than your machine depreciates, oil becomes a liability on your balance sheet — not just a lubricant in your tank.

Stand at the machine and watch the ram.

A conventional hydraulic cycles at 8–15 bends per minute depending on stroke and material. Modern electrics are advertising 15–25 bends per minute. Hybrids sit in between but closer to electric than old-school hydraulic. Faster approach, faster return, less dwell.

That’s not marketing fluff. It’s motor control.

When force is generated by servo-driven systems with closed-loop feedback, you get tighter position control at the bottom of stroke. Less overshoot. Less correction. Less time creeping into final angle. Ram parked at top dead center between bends with no pump churning beneath it.

Repeatability improves because you’re not compensating for oil temperature drift across a long shift. Anyone who has chased angle variation on a hot hydraulic system knows what that costs in scrap and rework.

Now tie that back to quoting. If your machine can reliably hit 18 bends per minute instead of 12, that’s a 50% theoretical throughput increase. You won’t capture all of it — material handling and operator pace matter — but even a 15–20% net productivity gain changes your per-part cost model.

Spec sheets used to revolve around tonnage and bed length. Now the sharper buyers are asking about acceleration curves, energy recovery, servo response time, and control openness.

Because once high tonnage is no longer exclusive to oil, the differentiator shifts.

And that shift is where the next margin battle will be fought.

Walk into any legacy OEM demo center and you’ll see the same pitch: proprietary CNC, vertically integrated tooling library, factory-certified service network. “One throat to choke.”

If electrics and hybrids now hit 320, 400, even 600 tons without breaking a sweat, this software stack is the last serious argument for sticking with conventional hydraulics. The claim is simple: the integration is tighter, the kinematics are tuned, the reliability is proven because it’s all one ecosystem.

Now imagine you’re a $40 million fab shop quoting tight-turn brackets for an EV supplier.

Your estimator pulls last year’s bend programs for 3/16 HSLA parts with four acute angles and two hems. Those bend deductions, springback compensations, and crowning corrections live inside a proprietary control that only one OEM’s service tech can legally extract in full fidelity. You can run the parts. You can’t freely migrate the process knowledge.

That’s not integration. That’s dependency.

When the machine was a hydraulic anchor bolted to the floor, that felt like stability. In 2026, with hybrid upstarts offering open-architecture controls that speak standard file formats and expose APIs to MES and ERP systems, that same lock-in starts to look like a margin leak you can’t see until it’s too late.

The question isn’t whether the OEM’s software works. It’s who owns the process intelligence after five years of production.

And that’s where the moat turns into a trap.

I’ve watched a 19-year-old with six weeks on the floor run parts he had no business touching—because the bends were simulated, collision-checked, and angle-verified offline before he ever touched the pedal.

Modern offline programming packages simulate tool selection, bend sequence, and interference in a 3D environment. You validate the program at a workstation, not at a 400-ton brake burning shop time at $185 per burdened hour. When the program hits the machine, it’s 90% there. Fine-tune the first article. Save. Move on.

That’s not theory. Shops using serious offline systems routinely cut tryout scrap and setup time because they’re not discovering collisions mid-cycle.

But here’s the part the brochures skip.

Robotic bending cells still see cycle penalties—on light-gauge, high-mix work, mobile setups can push close to a minute per bend once you factor in repositioning and part handling. If your software promises lights-out, but your mechanical choreography can’t keep up, your ROI model collapses under its own assumptions.

Software can compensate for a first-year operator on programming. It cannot compensate for bad cell design or throughput bottlenecks.

So where does that leave us?

If offline AI tools can level the operator skill curve across brands, then proprietary hydraulic ecosystems lose their “only our control can do this” edge. The skill moat shrinks. What matters becomes interoperability—can your bend data flow cleanly between CAD, offline programming, the brake, and your MES without custom middleware and paid unlocks?

Because once programming is portable, machine choice stops being about who guards the codebase and starts being about who integrates cleanly into your production stack.

The CapEx Reality: If AI-driven offline programming makes skill portable, then paying a premium for a closed control in the name of “operator advantage” is buying yesterday’s insurance policy.

A Danish fabricator I followed adopted an advanced clamping system that automated offsets for worn tools. They saved roughly 10 hours of milling time across six custom parts by letting the control adjust instead of re-machining fixtures. Smart move.

But about 30% of their clamping setups still required custom integration beyond the OEM’s standard software environment. Translation: real-world production didn’t fit neatly inside the proprietary box.

Now scale that.

Every time you introduce third-party tooling, a new vision system, or an MES upgrade, you’re asking: does the control expose the data I need, or does it gate it behind paid modules and factory permissions?

If your bend angle corrections, tonnage curves, and tool wear offsets live in a format only one OEM can fully access, you don’t own a production asset—you’re leasing your own process at a premium.

Open-architecture controls don’t magically solve integration. You still need competent IT and disciplined data management. But when the control speaks standard industrial protocols and allows structured export of bend parameters, you can:

That flexibility compounds over 10 years.

But scale cuts both ways.

Open systems expose your weaknesses too. If your shop floor data hygiene is sloppy, you’ll create chaos faster than a closed system ever could. The difference is choice. With proprietary ecosystems, you’re locked into the OEM’s roadmap and pricing. With open architecture, you carry more responsibility—but also more control.

Which matters more over a decade: convenience or ownership?

The CapEx Reality: When your bend database is trapped inside a proprietary CNC, the OEM controls your upgrade path, your integration costs, and—quietly—your negotiating leverage.

Picture a 320-ton hybrid with automatic tool change, angle measurement, and a robot tending light-gauge parts overnight. Ram parked at top dead center between cycles. No pump churning. Minimal idle draw. The hardware is ready.

The gating factor isn’t tonnage anymore. It’s data confidence.

Lights-out only works if the bend program is validated, the material variation is measured in real time, and the results feed back into the system without human babysitting. AI adaptive bending—using sensors to compensate for material variation—can reduce trial-and-error. But only if the control talks cleanly to the rest of the plant.

If that adaptive logic is proprietary and opaque, guess who captures the most value? The OEM selling service contracts, software upgrades, and locked modules to “enable” features already sitting in your cabinet.

If the architecture is open, the job shop captures the upside. You can integrate angle data into SPC dashboards. You can correlate springback shifts with specific material heats. You can refine your bend tables across brands.

That’s when lights-out stops being a marketing video and becomes margin expansion.

The final twist is uncomfortable.

Legacy hydraulic giants built their reputation on reliability measured in decades. Iron that lasts. Frames that don’t crack. That stability was a moat when the machine was mostly mechanical.

In a software-defined production environment, stability without openness is an anchor.

And anchors don’t move when tariffs spike on imported valves, when ESG reporting tightens, or when your EV customer demands real-time production data access as part of the contract.

So who benefits most when lights-out becomes real?

The shop that owns its data.

Or the OEM that licenses it back to you.

The CapEx Reality: In a world where tonnage parity is solved, software ownership—not hydraulic pedigree—is what determines who keeps the margin over the next 10 years.

In November, I watched a CFO green-light two 400-ton hybrid-electrics during a 120-day import surge window. The effective tariff rate had just dropped from north of 15% to the low teens after a court decision clipped some emergency powers. Everyone in the room acted like the pressure was off.

It wasn’t.

Section 301 on China is still sitting at 20%. Section 232 is still 25% on steel and aluminum, and by late 2025 it expanded into hundreds of derivative codes that catch industrial machinery components. Then a new Section 122 tariff layered another 10–15% on top. The headline rate moved. The stack didn’t disappear.

So when you evaluate a brake in 2026, you’re not just asking, “Is the control open?” You’re asking, “What’s the country-of-origin exposure on the servo drives, ball screws, CNC, and castings—and how fast can this OEM reroute supply if Washington sneezes?”

Because the shops that assumed “imported and assembled” would shield them learned the hard way that customs math doesn’t care about brochure language.

The CapEx Reality: If software ownership is your moat, tariff exposure is the tide level—ignore it and even the best control gets swamped by landed cost volatility.

I sat through a post-mortem where a 320-ton brake quoted at $412,000 landed closer to $487,000 after duties, brokerage, and reclassified components were reconciled. The sales rep kept saying, “Final assembly is domestic.”

Customs didn’t care.

Section 301 applies based on substantial transformation and component origin, not where the last bolt gets tightened. If the CNC, drives, or major subassemblies originate in a covered country, you’re exposed. When Section 232 expanded to cover more steel and aluminum derivatives, it hit the metal content inside the machine—frames, guards, brackets—while reciprocal tariffs tagged the rest. Layered duties. No marketing exemption.

And here’s the part nobody budgets for: pricing rigidity. Studies last year showed over 80% of small manufacturers faced significant tariff-driven price hikes, but very few rolled prices back when temporary relief hit. Once your supplier adjusts to a 25% duty environment, they build margin and contingency into the quote. Even if the effective rate drops a few points, the price doesn’t snap back.

So you’re left holding a machine whose BOM was inflated under peak-tariff assumptions, financed over seven years, while the OEM locks your software modules behind annual fees.

That’s not reliability. That’s compounding exposure.

The CapEx Reality: “Imported and assembled” is a customs classification strategy, not a margin strategy—and when duties stack, you pay on origin, not on slogans.

Walk the floor of a plant that truly pivoted, and you see it immediately. Weld fixtures for side frames built in-house. Servo cabinets wired locally. Domestic sourcing for hydraulic manifolds or, in the case of hybrid-electrics, for power electronics enclosures and busbars.

That’s expensive up front. I’ve signed checks north of $8 million to stand up fabrication cells just to control lead times. But once Section 232 started sweeping in more machinery-adjacent codes, the math changed. If your core frame and a meaningful chunk of your value-add are domestic, your exposure shrinks to specific imported components—not the entire machine value.

Here’s where agile upstarts moved faster than the legacy giants.

The global brands optimized for centralized casting, machining, and subassembly in Europe or Asia, then distributed worldwide. Re-shoring that footprint is like turning an aircraft carrier. Smaller players with modular designs and open controls could source drives from one region, frames from another, assemble in the U.S., and still keep their software architecture intact because it wasn’t tied to a single-country ecosystem.

But scale cuts both ways.

The big guys had volume leverage with suppliers. The smaller manufacturers had flexibility. When tariffs started hopping categories—first steel, then aluminum derivatives, then machinery investigations—the ones with diversified, swappable supply chains adjusted faster.

And faster adjustment means steadier pricing to the end user.

The CapEx Reality: The OEM that can shift 30–40% of its BOM across borders without rewriting its control stack is less likely to hand you a surprise change order six months after PO.

Let’s not kid ourselves. There are still scenarios where importing wins.

If a European-built 500-ton, 6-axis brake comes in with a base price $90,000 lower than a comparable domestic build, and your duty stack nets out to 13–15%, you might still be ahead on day one—especially if the dollar is strong and freight lanes are soft.

Now add context.

If that machine runs 2,200 hours a year at a burdened rate of $185 per brake hour, your annual revenue exposure tied to that asset is north of $400,000. One customs reclassification, one new machinery-specific 232 action, or one retaliatory move that adds 10% mid-cycle can wipe out the upfront delta in a single budget year.

And because price reductions rarely flow back downstream after tariffs ease, you don’t get the benefit on the way down. You just absorb the spike on the way up.

This is where software ownership and supply chain agility converge.

An open-architecture brake built with diversified sourcing lets you shift programs between a domestic 400-ton hybrid and an imported 320-ton electric if one line gets tariff-whiplashed. A closed ecosystem tied to a single global manufacturing hub turns that same machine into an anchor—bolted to your floor, dependent on one geopolitical lane.

Tariffs didn’t slow buying. I saw more POs signed during the 150-day window than in the prior quarter. They changed who felt safe signing them.

And the shops that feel safest now aren’t the ones buying the heaviest iron. They’re the ones buying flexibility—in code, in components, and in country of origin.

Because if EV and aerospace customers are about to demand tighter traceability, domestic content disclosures, and real-time data feeds, the question stops being “Where was it assembled?” and becomes “How fast can you adapt when the rules shift again?”

That’s not a trade policy question.

That’s a strategic one.

| Topic | Details |

|---|---|

| Core Question | Buying imported vs. domestic in 2026: when the landed cost equation still favors overseas sourcing |

| When Importing Wins | A European-built 500-ton, 6-axis brake priced $90,000 lower than a comparable domestic build, with a 13–15% duty stack, may still offer day-one savings—especially with a strong dollar and soft freight lanes. |

| Revenue Exposure Context | If the machine runs 2,200 hours annually at $185 per brake hour, revenue exposure exceeds $400,000 per year. A new customs reclassification, Section 232 action, or retaliatory 10% tariff mid-cycle can erase upfront savings within one budget year. |

| Tariff Asymmetry Risk | Price reductions rarely flow downstream after tariffs ease, meaning companies absorb cost spikes without benefiting from later decreases. |

| Software & Supply Chain Convergence | Open-architecture brakes with diversified sourcing allow program shifts between domestic and imported machines if tariffs impact one line. Closed ecosystems tied to a single global hub create geopolitical dependency. |

| Market Behavior During Tariff Window | Tariffs did not slow purchasing; more POs were signed during the 150-day window than the prior quarter. However, tariffs changed who felt secure making purchases. |

| What Feels Safe Now | The safest shops are not buying the heaviest equipment but investing in flexibility—software, components, and country-of-origin diversification. |

| Customer Demand Shift | EV and aerospace customers increasingly require tighter traceability, domestic content disclosures, and real-time data feeds, shifting focus from assembly location to adaptability. |

| Strategic Conclusion | The core issue is not trade policy but strategic adaptability when rules change. |

You want a practical way to evaluate tariff exposure and supply chain flexibility before signing a PO in 2026?

Start by asking a different question: what happens when your biggest customer suddenly wants titanium traceability down to the heat lot and ±0.0008-inch repeatability on a 12-foot part?

That’s not a customs problem. That’s a machine architecture problem.

A $40 million shop chasing EV battery enclosures and aerospace brackets can’t hide behind “proven” anymore. If your brake can’t document angle correction by material batch, log energy draw per cycle, and adjust springback in real time, you’re not just missing capability — you’re exposing margin. Because the OEM upstream is going to push that variability cost straight downhill to you.

The wildcard isn’t demand volume. It’s demand precision.

And precision is where the old anchor starts dragging.

Bend 6Al-4V titanium at 3/8-inch thick across a 10-foot bed and you learn humility fast. The material work-hardens, springback is aggressive, and tonnage spikes aren’t polite. A catalog 220-ton hydraulic with a standard 2-axis backgauge and generic crowning table was never designed for that dance.

You need dynamic crowning, real-time angle measurement, and a frame that doesn’t breathe under load. On big aerospace programs, that has meant custom 800-ton class hydraulics with adaptive forming systems — not because they’re nostalgic, but because they can hold consistent full-length pressure on massive parts where a smaller all-electric would tap out.

So no, hydraulics aren’t dead.

But look closer at what’s actually being bought. It’s not “off-the-shelf.” It’s custom-built, sensor-heavy, software-driven, and priced like a small building addition. The legacy badge is still on the side, but the machine is barely recognizable compared to the 2015 catalog version.

That’s the tell.

When even the hydraulic giants are winning contracts by engineering one-off adaptive systems instead of shipping standard frames, the old volume model is cracking. Agile builders saw that crack and moved faster in the 300- to 500-ton hybrid-electric range, where most EV structural parts and aerospace subcomponents actually live.

The CapEx Reality: If your work mix is drifting toward high-strength alloys and tight-tolerance parts, a stock-spec hydraulic isn’t “proven” — it’s under-spec’d for where your margins are heading.

It already is.

A landing gear supplier recently slashed 7075-T6 scrap by more than half using smarter tooling and springback compensation on existing brakes. No new frame. No shiny press release. Just better control of what was already there.

That should make you uncomfortable.

Because it proves the competitive gap isn’t always tonnage — it’s intelligence. If your control can’t store material-specific bend libraries, compensate per lot, and feed that data back into quoting, you’re eating variability that the sharper shop next door has already priced out.

And once aerospace demands that data discipline, EV follows.

Battery tray sidewalls in 980 MPa steel don’t forgive sloppy angle drift. Neither do structural aluminum extrusions in a lightweight chassis program. The tolerances that used to live only in AS9100 shops are creeping into mainstream fabrication because OEMs are squeezing weight and energy efficiency everywhere they can.

But scale cuts both ways.

The shops that invested in open controls and modular upgrades can retrofit angle measurement, add 6-axis backgauges, and integrate offline programming without scrapping the entire asset. The shops locked into closed hydraulic ecosystems are staring at full replacements to get the same data transparency.

The CapEx Reality: Micron-level repeatability isn’t a niche tax anymore — it’s becoming the entry fee, and whether you can bolt it on or must buy it all over again decides your real exposure.

Let’s be honest: ESG reporting is part of it. I’ve seen RFQs that ask for machine energy consumption per cycle and standby draw as line items, like we’re bidding solar panels.

An all-electric brake with servo-driven ball screws will idle at a fraction of the kW draw of a traditional hydraulic with the motor spinning and oil circulating. That matters when your customer is calculating Scope 2 emissions and wants a tidy spreadsheet.

But the performance edge is where the conversation gets serious.

Electrics and hybrids deliver peak force on demand. No warm-up drift. No oil viscosity games in February. Ram position control down to microns because you’re measuring motor rotation directly, not inferring movement through hydraulic pressure. On thin-gauge stainless and aluminum — which make up a lot of EV enclosure work — that translates into faster cycle times and fewer angle corrections.

Now flip the coin.

On very thick, long, high-tonnage titanium sections, a well-engineered hydraulic or hybrid still wins for sustained, uniform pressure across the bed. That’s why certain flagship aerospace projects continue to spec massive adaptive hydraulics. Physics doesn’t care about marketing decks.

So EV supply chains aren’t blindly ditching oil. They’re selecting architectures based on part mix, data requirements, and energy transparency.

And that selection process exposes the trap.

If you buy a legacy hydraulic because it’s “what we’ve always run,” then discover two years later that your EV customer wants machine-level energy logs, API access to bending data, and tighter angle documentation, you’re not negotiating from strength. You’re negotiating from retrofit.

The CapEx Reality: ESG may open the door for all-electric and hybrid brakes, but the real advantage is data-rich, repeatable performance — and if your machine can’t prove what it did, “proven reliability” stops being a selling point and starts being a liability.

You structure it around optionality, not horsepower.

That’s the shift. The wrong move in 2026 isn’t buying hydraulic or electric. It’s buying a closed asset that assumes your part mix, your customer data demands, and your compliance burden will stay politely frozen for the next seven years.

I’ve signed off on enough 400- to 800-ton purchases to know this: the frame is the cheapest long-term mistake you can make. Software lock-in, proprietary angle systems, non-exportable bend data — those are the gifts that keep charging you. If the control can’t push bend data to your MES, log energy per cycle, and accept third-party upgrades without a factory tech and a five-figure invoice, you didn’t buy a press brake. You bought dependency.

So restructure CapEx like this: buy bending capacity in modular layers. Frame and tonnage sized for your 80% work. Open control architecture as non-negotiable. Sensor packages that can be upgraded without replacing the backbone. Regional strategy if you run multiple plants — hydraulics where grid stability and service density favor them, hybrids where ESG and precision reporting drive margin.

You’re not buying steel and cylinders anymore. You’re buying adaptability over 84 months.

The question is where the money actually hides.

Everyone wants a clean answer: “retrofit is cheaper” or “replace is future-proof.” Reality is uglier.

If you’ve got a 600-ton hydraulic with a rigid frame and decent crowning, retrofitting angle measurement and a modern CNC can absolutely extend life. I’ve seen shops cut scrap in half on 7075 just by adding closed-loop angle feedback and better springback compensation. No new iron. That’s real ROI.

But here’s the mechanism that kills the math: integration friction.

If the OEM locks the hydraulic valve block, if the control won’t export bend data without a paid middleware layer, if adding a 6-axis backgauge requires proprietary firmware, your “$180,000 upgrade” becomes $310,000 by the time you’re done — and you still have a 15-year-old pump drawing power all shift.

Now flip it. A 320- to 400-ton hybrid-electric with open APIs, servo-driven backgauge, and energy logging built in might run higher upfront. But if it eliminates oil maintenance, reduces warm-up scrap, and feeds live bend data into quoting, the payback isn’t just kWh. It’s tighter standard times and fewer surprise reworks at $185 per burdened brake hour.

Hydraulics still own high-volume stability in a lot of sheet work. That 52% global share exists for a reason. On repetitive, thick-gauge runs, a well-maintained hydraulic can be brutally consistent. But the ROI question isn’t “does it bend reliably?” It’s “can it evolve without a forklift?”

The CapEx Reality: Retrofit only wins if the underlying machine can accept modern intelligence without proprietary toll booths. If it can’t, replacement isn’t extravagance — it’s damage control.

Which leads to the fear everyone has about newer builders.

I don’t care how pretty the HMI looks if the company disappears in year five.

But stability isn’t just age. It’s structure.

The legacy giants with vertical integration — hydraulics, controls, service network under one roof — have a real moat. They can evolve hybrids without losing parts support. That’s why some of them are still winning with electric and hybrid lines that undercut the “agile upstart” narrative.

So how do you vet a newer brand without betting your plant on hope?

Start with parts independence. Are the servo drives standard industrial units or custom boards only they can supply? Is the control built on a widely supported platform, or something only their factory can touch? If your ram is parked at top dead center and the control dies, can you source a replacement through normal industrial channels?

Then service density. Not brochure claims — actual technicians within a day’s drive. Ask for customer references in your tonnage class, not their flagship install.

And finally, financial posture. Are they selling machines or ecosystems? A builder making margin on software subscriptions and service contracts is incentivized to stay alive and maintain compatibility. One surviving on razor-thin hardware margins is vulnerable the moment tariffs or currency shift.

The trap isn’t new brands. The trap is buying from anyone — old or new — whose business model requires you to stay dependent.

The CapEx Reality: Stability isn’t about logo age; it’s about whether the machine’s critical components and software can outlive the vendor.

Which changes the last question entirely.

Biggest used to mean safest. Biggest frame. Biggest installed base. Biggest badge.

But scale cuts both ways.

Large OEMs can absorb tariff swings and fund R&D. They can also lock you into closed ecosystems that meter every upgrade. Smaller builders can move fast and embrace open architecture. They can also vanish if capital dries up.

So stop asking who dominates tonnage charts. Ask who controls your cost per bend over the next 84 months.

Break it down:

Now imagine you’re a $40 million fab shop quoting tight-turn brackets for an EV supplier. The RFQ asks for energy reporting, lot-level traceability, and ±0.001-inch repeatability across shifts. If your brake can produce the part but not the proof, you’re discounting price to compensate for risk.

That’s margin erosion disguised as reliability.

The one thing to carry forward is this: the machine that gives you the most control over data, upgrades, and operating inputs will out-earn the machine that simply delivers the most tonnage. That’s non-obvious because for 30 years, mass and brand were proxies for safety.

They aren’t anymore.

You’re not buying an anchor to bolt to the floor. You’re choosing whether your bending department can pivot as precision, ESG, and customer audits tighten the screws.

The shops that treat CapEx as a flexibility strategy will maneuver.

The ones that treat it as a horsepower contest will feel the drag.